On Thursday, June 22, 2017, Senate Majority Leader Mitch McConnell of Kentucky released a 142-page healthcare “Discussion Draft” of legislation, called the Better Care Reconciliation Act of 2017 (BCRA), which is the Senate version of the Affordable Care Act (ACA) “repeal-and-replace” legislation American Health Care Act (AHCA) passed by the U.S. House of Representatives last month. An updated “Discussion Draft” of the BRCA was released on June 26, 2017. A summary of the updated June 26 draft of the BCRA by the U.S. Senate Committee on the Budget is available here and a section-by-section summary of the June 26th version is available here.

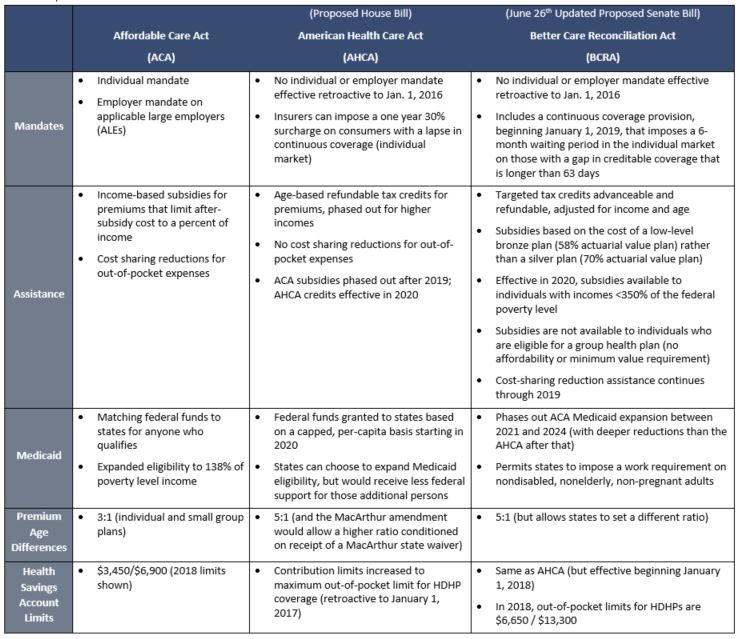

The major substantive change in the updated Discussion Draft released on June 26 was to add a new Section 206, beginning in 2019, that would subject an individual who has a break in continuous “creditable coverage” for 63 days or more in the prior year to a six-month waiting period (in the individual market) before coverage begins. This provision is intended to provide an incentive for young and healthier individuals to maintain health insurance since the bill would eliminate the individual mandate. The AHCA proposed imposing a 30% surcharge on those without continuous creditable coverage, but there were concerns over whether that provision could pass Senate parliamentary rules.

The unveiling of the Senate bill comes after weeks of drafting by a small group of Senate Republican leadership behind closed doors that has frustrated Democrats and left out many Republicans from the drafting process. The Congressional Budget Office released its score of the legislation on June 26, 2017, finding that the updated Discussion Draft of the BCRA would leave 22 million more uninsured by 2026 than under the ACA (versus 23 million under the AHCA). Senator McConnell is pushing for a Senate vote by the end of this week before the Fourth of July recess. It is unclear whether the Republicans will be able to secure enough votes to pass the bill because at least five Republican senators – Sens. Rand Paul (KY), Ron Johnson (WI), Mike Lee (UT), Ted Cruz (TX), and, most recently, Dean Heller (NV) – have publicly expressed their unwillingness to vote for it as currently drafted. Other senators are still reviewing but have expressed concerns (e.g., Senator Rob Portman of Ohio regarding the Medicaid policies and Senator Mike Rounds of South Dakota on group market issues).

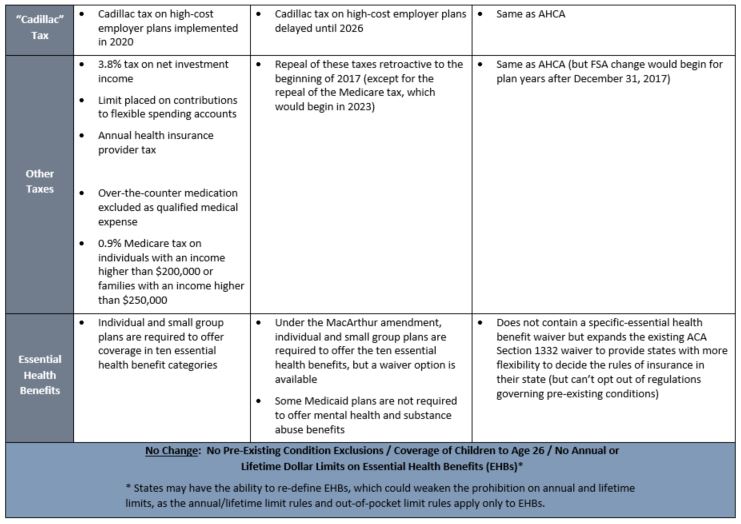

In large part, the BCRA mirrors the House-passed AHCA. A comparison of the two bills can be found below. Similar to the House bill, the Senate bill would repeal virtually all of the tax increases imposed by the ACA, except for the “Cadillac” tax on high-cost employer-sponsored coverage, which would be delayed through 2025.

Key Issues for Employers

For employers, the most significant change made by the AHCA to the ACA that was retained by the BCRA is the repeal of the employer mandate penalties effective January 1, 2016. The BCRA retains other significant AHCA changes for employers, including unlimited flexible spending accounts, and enhancements to health savings accounts (HSAs). Of note for employers sponsoring fully-insured group health plans, beginning in 2020 the bill requires states to set their own medical loss ratio rebating rules. It also adds a structure under ERISA (by adding a new Part 8) that would allow for the establishment of association health plans for small businesses or individuals (Small Business Health Plans or SBHPs), allowing them to be treated as large group plans exempt from the community rating and essential health benefit requirements that are currently applicable to small group and individual plans. This new section of ERISA would preempt any and all state laws that would preclude an insurer from offering coverage in connection with an SBHP and would go into effect one year after enactment (and implementing regulations would be required to be promulgated within six months of enactment).

The addition in the updated June 26th Discussion Draft of a continuous coverage requirement would again require employers to provide written certifications of periods of creditable coverage for the purpose of verifying that the continuous coverage requirements are met.

Also significant is that the bill does not include a provision capping the tax exclusion for employer provided health insurance. Many employers were concerned that the exclusion would be capped or removed as a way to increase revenue to pay for other tax cuts in the bill. Nor does the bill repeal the Sections 6055 and 6056 reporting requirements. It will remain to be seen whether, if the BCRA is passed, the IRS may continue to use the existing ACA information reporting system to determine whether an individual is eligible for a premium tax credit or is prohibited from receiving one in 2018 or 2019 because such an individual has an offer in 2018 or 2019 of affordable, minimum value employer-sponsored coverage. Or, whether in 2020 and thereafter, the IRS would need information to assess whether an individual has any offer of employer-sponsored coverage to determining eligibility for the premium tax credit.

Key Issues for Individuals

For individuals, the BCRA would repeal the ACA’s Medicaid expansion, but at a slower rate than proposed by the AHCA and would tighten the eligibility criteria for premium subsidies (beginning in 2020, only those earning up to 350% of the poverty level would qualify rather than the 400% threshold in the ACA); however, subsidies would open up for enrollees below the poverty level living in states that did not expand Medicaid. The bill would allocate money for cost-sharing subsidies through 2019, which are used to offset the costs for insurers to offer low-income individuals with coverage that has lower out-of-pocket costs. There had been uncertainty whether these payments would continue, which was causing instability in the individual insurance market. Higher-income individuals would see relief from various ACA taxes and fees, including the 0.9% Medicare surtax beginning in 2023 and the 3.8% net investment income tax retroactive to the beginning of this year.

Next Steps

The Republicans are trying to pass the bill through the budget reconciliation process since it allows them to avoid a Democratic filibuster and to pass the bill with a simple majority (rather than 60 votes). However, the Republicans have only 52 Senate seats, which means that to pass, Senator McConnell can only afford to lose 2 votes (Vice President Pence can be the tie breaker). The bill may be too liberal for some Republican senators and too “harsh” for others (the CBO score released on June 26th states that the BCRA would leave 22 million more uninsured by 2026 than under the ACA), so it remains to be seen whether the bill, as proposed, will pass or whether it will undergo further revisions to ensure passage. Currently, there are at least 5 Republican senators who have publicly expressed that they would not vote for the bill as currently drafted. The Republicans will not have much time to sort out any disagreement since Senator McConnell has stated that he intends to call a vote this week before the July 4th recess.

If the Senate passes a bill, it will either have to be approved by the House (the two chambers would have to reconcile their differences in a conference committee), or the House could pass a new version and send it back to the Senate for approval.

As noted previously, employers and other stakeholders should continue to stay the course on ACA compliance at this time while they monitor for changes as the BCRA continues to make its way through the legislative process.

Comparison of the ACA, AHCA, and BCRA

The chart below compares some of the significant changes proposed by the BCRA to the ACA and the proposed House bill.

About the Author

This alert was prepared for Benefit Advisors Network by Stacy Barrow. Mr. Barrow is a nationally recognized expert on the Affordable Care Act. His firm, Marathas Barrow Weatherhead Lent LLP, is a premier employee benefits, executive compensation and employment law firm. He can be reached at sbarrow@marbarlaw.com.

This message is a service to our clients and friends. It is designed only to give general information on the developments actually covered. It is not intended to be a comprehensive summary of recent developments in the law, treat exhaustively the subjects covered, provide legal advice, or render a legal opinion.

Benefit Advisors Network and its smart partners are not attorneys and are not responsible for any legal advice. To fully understand how this or any legal or compliance information affects your unique situation, you should check with a qualified attorney.

© Copyright 2017 Benefit Advisors Network. Smart Partners. All rights reserved