On December 22, 2017, President Trump signed what is popularly known as the Tax Cuts and Jobs Act (H.R. 1) (the “Bill”), overhauling America’s tax code for both individuals and corporations and providing the most sweeping changes to the U.S. Tax Code since 1986. The House and Senate Conference Committee provided a Policy Highlights of the major provisions of the Bill, and the Joint Committee on Taxation provided a lengthy explanation of the Bill.

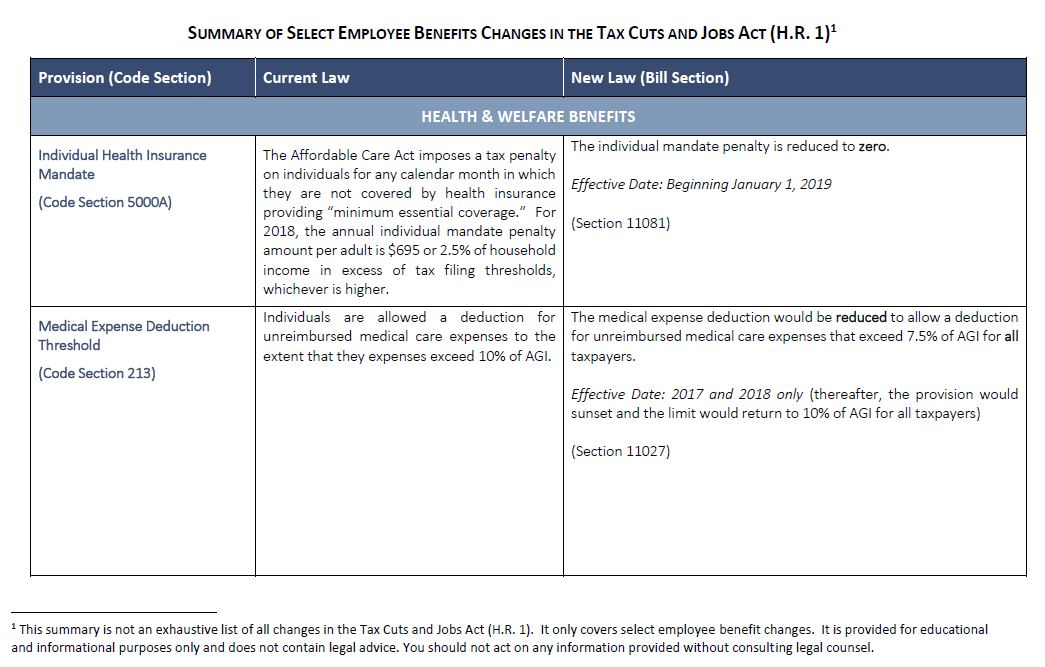

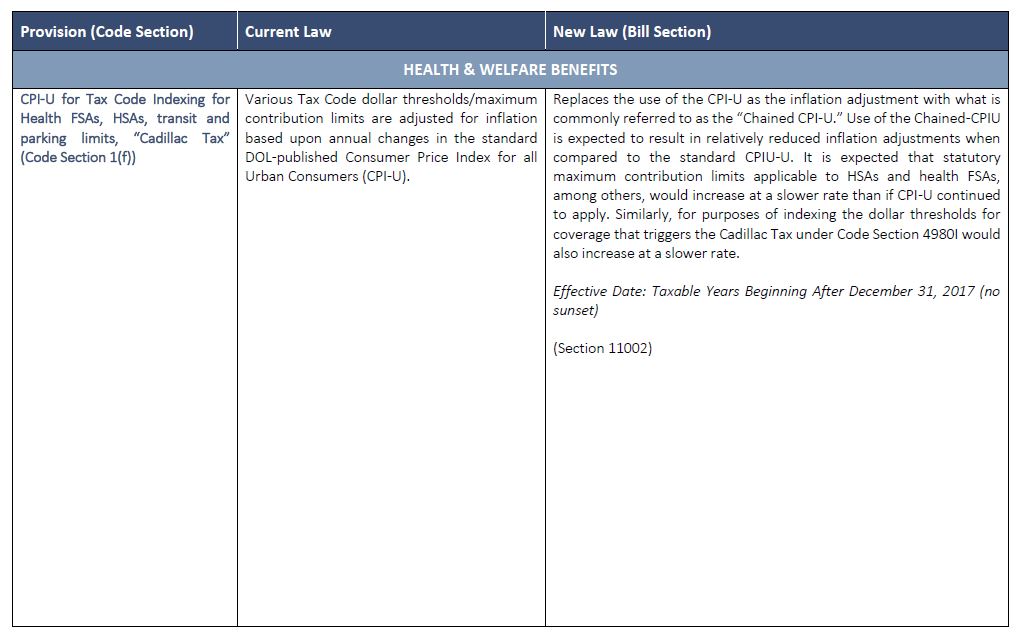

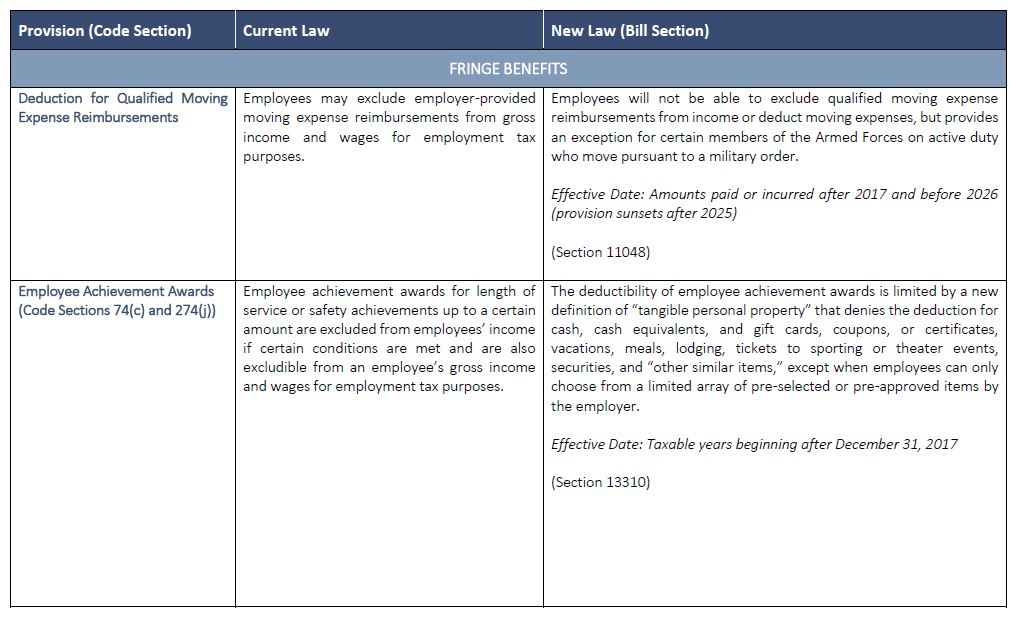

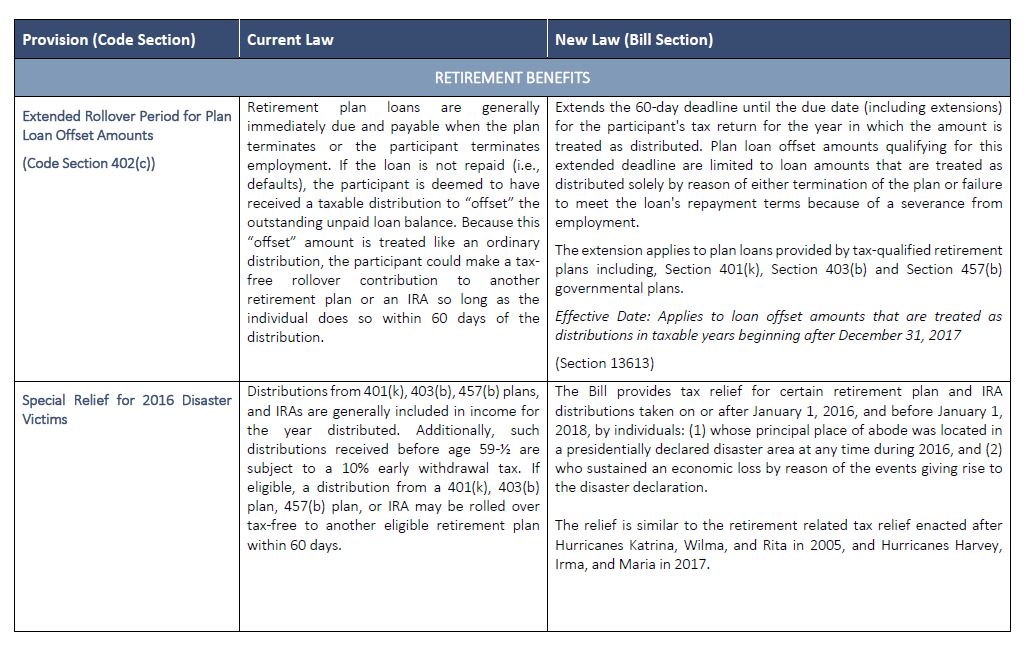

Compared to initial proposals, the final Bill generally does not make significant changes to employee benefits. The chart that follows highlights certain broad-based health and welfare, fringe and retirement plan benefit provisions of the Bill (comparing them to current law). Notable changes include:

- Repeal of the Individual Mandate penalty beginning in 2019;

- Elimination/changes of employer deductions for certain fringe benefits, including qualified transportation fringes, moving expenses, and meals/entertainment;

- New tax credit for employers that pay qualifying employee while on family and medical leave, as described by the Family Medical Leave Act;

- Extended rollover periods for deemed distributions of retirement plan loans; and

- Tax relief for retirement plan distributions to relieve 2016 major disasters.

In addition, the Bill makes certain narrowly-tailored changes (which we did not include in the chart that follows) impacting only certain types of employers or compensation. For instance, the Bill:

- Modifies the $1 million compensation deduction limitation under Code Section 162(m) for publicly traded companies (expanding the type of compensation which will be applied against the limitation, the individuals who will be considered covered employees, and the type of employers that will be subject to the limitation), with transition relief for certain performance-based compensation arrangements pursuant to “written binding contracts” in effect as of November 2, 2017, so long as such arrangements are not “modified in any material respect”; and

- Creates a new “qualified equity grant” by adding a new Code Section 83(i), which allows employees of non-publicly traded companies to elect to defer taxation of stock options and restricted stock units (“RSUs”) for up to five years after the exercise of such stock options or the vesting of RSUs.

The Bill also has specific provisions impacting employers that are tax-exempt organizations. For instance, it imposes a new excise tax for highly compensated non-profit employees, and changes the way non-profits calculate unrelated business income tax (UBIT).

What’s Not Changing

ACA Employer Mandate & Reporting

While the individual mandate penalty has been reduced to zero beginning in 2019, at this time, the employer mandate and employer reporting requirements under the Affordable Care Act (ACA) remain in effect.

In addition, there were no changes to other ACA taxes and requirements. For example, the bill does not eliminate (or delay) the 40% excise tax on high-cost plans (Cadillac Tax) that is scheduled to be effective beginning in 2020, nor does it eliminate the comparative effectiveness research fees paid annually to fund the Patient-Centered Outcomes Research Institute (PCORI) through 2019. However, the Trump Administration has indicated its intention to renew ACA repeal and replace efforts in 2018, which may result in additional changes at a later date.

It has been recently reported that Republican legislators are targeting a further delay of two ACA-created taxes – a 2.3% excise tax on medical devices, and an annual fee imposed on health insurers known as the HIT tax – for inclusion in a spending bill that must be passed by January 19. Both of these taxes are scheduled to go into effect beginning in 2018 after a delay was incorporated in a 2015 year-end tax extenders deal. Employer groups have been lobbying for an elimination or delay of the Cadillac Tax and relief on the employer mandate. It remains to be seen whether these tax relief items will be included as part of a spending bill later this month.

FSAs, HSAs, Adoption Assistance and Education Assistance Programs

Earlier versions of the Bill in both the House and Senate included provisions that would have significantly impacted the tax treatment of many employee benefits. However, the final Bill makes no changes to the tax treatment of HSAs, dependent care FSAs, health FSAs, adoption assistance programs, or qualified education assistance programs. Although, it has been reported that repealing restrictions on using FSAs, HSAs and other account-based plans to purchase over-the-counter medications could also be considered during negotiation of the spending bill.

Unsubsidized/Pre-Tax Qualified Transportation Fringe Benefits

While the Bill eliminated the employer deduction for qualified transportation fringe benefits, this change would appear to have the most impact on employers who subsidize transit and parking expenses since they may no longer claim a deduction for subsidized transit expenses (but such amounts would still be exempt for payroll tax purposes). For the majority of employers who do not subsidize transit expenses but offer pre-tax qualified transportation fringe programs that allow employees to enter into salary reduction agreements and receive transit expense reimbursements on a tax-free basis, the Bill should not have an impact on those programs. Tax-exempt employers will be taxed on the value of providing qualified transportation fringe benefits (such as payments for mass transit) by treating the funds used to pay for the benefits as UBIT.

For the majority of employers who do not subsidize transit expenses but offer pre-tax qualified transportation fringe programs that allow employees to enter into salary reduction agreements and receive transit expense reimbursements on a tax-free basis, the Bill should not have an impact on those programs. Employees may continue to receive transit expenses (other than bicycle commuting expenses) on a tax-free basis under such programs.

Structural Changes to Qualified Retirement Plans and Deferred Compensation Plans

In addition, there were no major changes to the general structure of qualified retirement plans, such as the “Rothification” of pre-tax deferrals in 401(k) plans, nor reductions in the limits that could be contributed tax-free. Nor were other changes that were initially proposed in the House version of the bill to retirement provisions (e.g., changing the minimum age of in-service distribution in retirement plans, modifying non-discrimination rules for “soft-frozen” defined benefit plans, and changes to 401(k) and 403(b) hardship withdrawal rules) included in the final bill.

Earlier versions of the Bill would have also completely upended how deferred compensation by companies to executives is paid by taxing such compensation when it vested. But this provision did not survive in the final Bill.

Next Steps

Only time will tell the full impact of the Bill on employers and employees. For instance, the repeal of the individual mandate beginning in 2019 may result in fewer “healthy” individuals enrolling in health coverage, resulting in increased premiums. Fewer individuals may enroll in Exchange coverage, reducing potential employer mandate penalty (both “A” and “B”) exposure, which is triggered when a full-time employee receives a premium subsidy for Exchange coverage.

Given the changes to the corporate tax rates, it remains to be seen whether employers will alter how they compensate their employees, particularly, highly compensated employees, and how they will handle their pension, 401(k)/profit sharing plans, and other employee benefits.

In addition, it is likely that there will be a correction bill (and IRS guidance) in 2018 to address unintended consequences, omissions, ambiguities, and drafting errors in the Bill. We will continue to monitor for further legislative and other developments impacting employee benefits as a result of the passage of the Bill.

In the meantime, we suggest that employers work with their payroll departments and vendors, accountants, finance, counsel and other advisors to assess the impact of the Bill to its benefit programs and implement necessary changes to their systems and practices.

About the Authors

This alert was prepared for Benefit Advisors Network by Marathas Barrow Weatherhead Lent LLP, a national law firm with recognized experts on the Affordable Care Act. Contact Peter Marathas, Stacy Barrow or Tzvia Feiertag.

This message is a service to our clients and friends. It is designed only to give general information on the developments actually covered. It is not intended to be a comprehensive summary of recent developments in the law, treat exhaustively the subjects covered, provide legal advice, or render a legal opinion.

Benefit Advisors Network and its smart partners are not attorneys and are not responsible for any legal advice. To fully understand how this or any legal or compliance information affects your unique situation, you should check with a qualified attorney.