With the tight labor market and new generations in the workforce, the C-suite should be asking what they can do to remain relevant.

Written by Perry Braun, Executive Director of Benefit Advisors Network, and Bobbi Kloss, Director of Human Capital Management Services. BenefitsPro.com, February 11th, 2019.

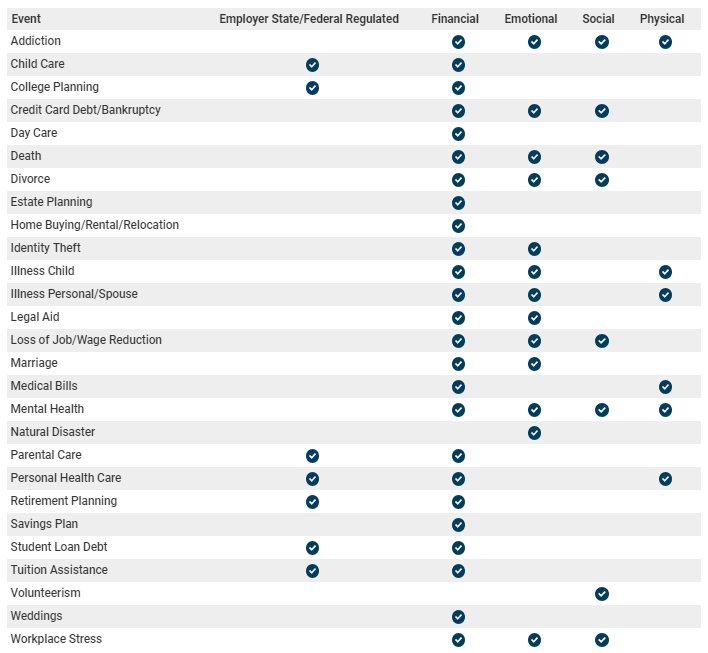

Life happens. Things happen every day that we rarely give a second thought to as we go about our daily routines.

High impact life events are another story. Not only do they disrupt our daily routine, but they can stop us dead in our tracks and affect every aspect of our lives: physically, emotionally, financially and even socially. Even planning for an expected event can seem to be overwhelming and disruptive.

Holistic Wellness – High Impact Life Events

When a high impact life event happens to an employee, the effects can ripple throughout the workplace. The distractions of the event can cause performance issues, absenteeismand presenteeism. Supervisors and HR traditionally have dealt with these issues through corrective actions, up to and including termination of employment. But changing workforce dynamics show us why employers need… [Read More]

On November 15, 2018, the Internal Revenue Service (IRS) released Revenue Procedure 2018-57, which raises the health Flexible Spending Account (FSA) salary reduction contribution limit by $50 to $2,700 for plan years beginning in 2019. The Revenue Procedure also contains the cost-of-living adjustments that apply to dollar limitations in certain sections of the Internal Revenue Code.

Qualified Commuter Parking and Mass Transit Pass Monthly Limit Increase

For 2019, the monthly limits for qualified parking and mass transit are $265 each (up $5 from 2018).

Adoption Assistance Tax Credit Increase

For 2019, the credit allowed for adoption of a child is $14,080 (up $270 from 2018). The credit begins to phase out for taxpayers with modified adjusted gross income in excess of $211,160 (up $4,020 from 2018) and is completely phased out for taxpayers with modified adjusted gross income of $251,160 or more (up $4,020 from 2018).

Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) Increase

For 2019, reimbursements under a QSEHRA cannot exceed $5,150 (single) / $10,450 (family), an increase of $100 (single) / $200 (family) from 2018.

Reminder: 2019 HSA Contribution Limits and HDHP Deductible and Out-of-Pocket Limits

Earlier this year, the IRS announced the inflation-adjusted amounts for HSAs and high deductible health plans (HDHPs).

The ACA’s out-of-pocket limits for in-network essential health benefits have also increased for 2019. Note that all non-grandfathered group health plans must contain an embedded individual out-of-pocket limit within family coverage if the family out-of-pocket limit is above $7,900 (2019 plan years). Exceptions to the ACA’s out-of-pocket limit rule are also available for certain small group plans eligible for transition relief (referred to as “Grandmothered” plans). Unless extended, relief for Grandmothered plans ends December 31, 2019.

The table below describes penalties related to returns filed in the applicable year (e.g., the 2019 penalty is for returns filed in 2019 for calendar year 2018). Note that failure to issue a Form 1095-C when required may result in two penalties, as the IRS and the employee are each entitled to receive a copy (increased for willful failures, with no cap on the penalty).

About the Author. This alert was prepared for Benefit Advisors Network by Stacy Barrow. Mr. Barrow is a nationally recognized expert on the Affordable Care Act. His firm, Marathas Barrow Weatherhead Lent LLP, is a premier employee benefits, executive compensation and employment law firm. He can be reached at sbarrow@marbarlaw.com.

This message is a service to our clients and friends. It is designed only to give general information on the developments actually covered. It is not intended to be a comprehensive summary of recent developments in the law, treat exhaustively the subjects covered, provide legal advice, or render a legal opinion.

Benefit Advisors Network and its smart partners are not attorneys and are not responsible for any legal advice. To fully understand how this or any legal or compliance information affects your unique situation, you should check with a qualified attorney.

Prehypertension and Hypertension (“HTN”) are important issues for health plans, providers, and individuals. Because of high prevalence, the potential for dangerous costly complications, and the availability of effective treatments, HTN has been an important “target” for guideline development.

Key facts illustrating the importance of HTN for costs and health status are:

HTN is common: In the U.S. 80% of men and 85% of women over 75 years of age have HTN. Nearly 1 billion individuals worldwide have Stage 2 hypertension (the most severe stage).

Because of the increasing prevalence of risk factors for HTN (such as inactivity and overweight/obesity), the prevalence and consequences of HTN are expected to increase.

HTN is the second (after smoking) most important condition driving preventable deaths in the U.S.

HTN is a leading risk factor for downstream conditions (coronary artery disease, heart failure, stroke and kidney failure) that result in significant costs, morbidity, mortality, and disability.

The probability of developing a dangerous downstream condition increases in direct relationship to increasing blood pressure.

Although direct diagnosis and treatment (drug) costs related to HTN itself are relatively low, costs for significant conditions caused by HTN (for example, renal failure and dialysis or rehab and nursing home care after a stroke) hypertension are high, and significant disability often results.

There is now convincing evidence that adequately controlling blood pressure in individuals with HTN results in decreases in the incidence of complications of the disorder.

Guideline Summary

A new national guideline for detection, evaluation, and treatment of high blood pressure[1] has just been published. As a new national evidence-based standard, the new guideline will have a major impact on the ways in which HTN is diagnosed and treated.

Because of the complexity of the (200 page) guideline, adoption will most likely be incremental, occurring over several years. We anticipate that health plans, providers, and disease management and biometric screening firms will “readjust” their HTN norms.

In general, the guideline establishes new (lower) blood pressure targets for diagnosis and treatment of HTN and adds new treatment modalities, including lifestyle modification for individuals just above the BP threshold. Consistent with the new cholesterol treatment guidelines; the cardiac risk score is now a mandatory factor in deciding whether to institute drug treatment.

Another important change is the recommendation for ambulatory home continuous BP monitoring as a component of the diagnosis and monitoring of HTN.

These changes have important health management and financial implications for both brokers and employers.

What are the Specific Changes?

The most important changes in the new guideline are:

Lowering of the threshold for diagnosis of prehypertension (elevated BP) and HTN.

Elimination of a higher HTN threshold for older adults.

Lowering of the “treatment target” BP.

Addition of ambulatory (home) BP monitoring as recommended diagnostic and disease management service for the diagnosis and treatment of elevated BP and HTN.

Addition of lifestyle modification as a strongly recommended treatment modality.

What are the Implications for Brokers and Employers?

The guideline will result in major changes in the diagnosis and treatment of HTN. These changes have important implications for employer groups:

The “baseline” is being reset (to 120/80). Because of a lower threshold for diagnosis of elevated blood pressure, it is estimated that the new guideline will result in 46% of adults carrying a diagnosis of elevated BP or HTN. This will make comparison (to prior period values) of new biometric, utilization, drug use, and diagnosis-related cost data difficult.

Application of the new treatment guidelines will result in an additional 2% (or more) of all adults (4.2 million individuals in the U.S.) receiving drug treatment for elevated blood pressure. Plans with “maintenance drug” member cost share forgiveness will experience higher cost increases than plans with “standard” formulary designs.

Because of the complexity of the new guidelines and inclusion of factors that cannot be abstracted from claims data (for example, cardiac risk), some gaps in care metrics (for HTN) will become more difficult or impossible to quantify. Some gap scores will not be comparable to prior periods.

Ambulatory (home) blood pressure monitoring is now recommended as a routine important/essential procedure for treatment-monitoring for all patients with suspected or existing HTN. This will cause increases in professional and medical equipment costs for diagnosis and treatment of HTN in adults. Coverage and member cost share issues will need to be addressed.

Telemedicine is now recommended as an adjunct to home monitoring in adults with established HTN. Coverage and member cost share issues will need to be addressed. Plans not currently offering a telemedicine benefit may need to consider doing so.

Lifestyle risk factor modification is an intrinsic treatment component of the new guideline for all individuals with BP >120/80. This may result in increased costs due to increased demand for health plan or 3rd party vendor services.

If a 3rd party (lifestyle, risk, or disease management vendor contract is in place, contract terms may change. The likelihood of this occurring will depend on existing vendor contract terms.

Until health plans “catch up” with the new guidelines, members may receive denials for home monitoring and telemedicine costs. We would expect increases in member appeals and the communication “burden” on employers.

In summary, Employers and Brokers should expect that an increased percentage of members will be diagnosed with preHTN or HTN, that costs for diagnosis and treatment of members with these disorders will rise, and that additional diagnostic and treatment services will need to be covered by plans.

Background: Guideline Development

Since 1977, HTN diagnosis and treatment guidelines have been developed and published by the Joint National Committee on Detection, Evaluation, and Treatment of High Blood Pressure (the “JNC”). Members of this Committee have historically been appointed by the National Heart, Lung, and Blood Institute (“NHLBI”; part of the National Institutes of Health).

The most recent comprehensive Blood Pressure guideline (JNC7) was published in 2003. The JNC began work on modifications to this guideline (“JNC7”) in 2008. In 2013, before the final updated guideline was published, NHBLI disbanded the JNC and transferred responsibility for development of CVD prevention guidelines to the American Heart Association and the American College of Cardiology.

In 2014, the AHA and ACC (in partnership with nine other professional societies) began work on a new national blood pressure guideline. The ACC/AHA 2017 guideline has now been published (November 2017), and is the most comprehensive BP guideline since JNC7 and modifications to it proposed (but never universally adopted) in the 2008 – 2013 time-frame.

[1] High Blood Pressure: hypertension or “HTN”.

About the Author

Dr. Bruce Campbell is the Chief Medical Director of BAN, where he brings over 25 years of executive experience in healthcare, information technology, and managed care to the membership.

He has held executive staff and operating positions in healthcare services companies, managed care plans, integrated delivery systems, medical groups, and healthcare information technology companies. His background includes having served as a Senior Vice President of Operations and the Chief Medical Officer of a national managed care company, and tenure as the Chairperson of the Audit Committee of the Board of Directors of a public company operating Medicare Special Needs Plans and disease management programs.