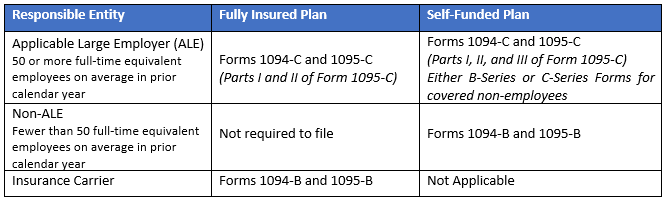

On September 27, the Internal Revenue Service (IRS) released proposed regulations on the application of the Affordable Care Act’s (ACA) employer shared responsibility provisions to a new type of Health Reimbursement Arrangement (HRA) available starting in 2020. In June 2019, the Department of Labor, the Department of Health and Human Services, and the Treasury Department (the “Departments”) released a final rule concerning HRAs that can be integrated with individual market coverage or Medicare. This new type of HRA is referred to as an Individual Coverage HRA, or ICHRA. The rule, based on an executive order from President Trump in 2017, is intended to increase the usability of HRAs, to expand employers’ ability to offer HRAs to their employees, and to allow HRAs to be used in conjunction with non-group coverage.

The ICHRA rule is effective for plan years beginning on or after January 1, 2020. The IRS has also proposed regulations to guide employers in determining whether their contribution to an employee’s ICHRA results in an “affordable” offer of coverage under the ACA. Specifically, the proposed regulations will assist employers who offer ICHRAs in determining the “required employee contribution” for purposes of line 15 of Form 1095-C. Employers may continue to use the W-2, Rate of Pay, or Federal Poverty Level safe harbors to determine whether their entry in line 15 results in an “affordable” offer of coverage. (See Example on page 3.)

The proposed regulations are effective for periods after December 31, 2019. Employers may continue to rely on them during any ICHRA plan year beginning within six months from the publication of any final regulations.

Proposed Safe Harbors

The proposed regulations offer safe harbors for applicable large employers (ALEs), which are those who employed at least 50 full-time equivalent employees on average in the prior calendar year. When an employer offers an ICHRA to a full-time employee, the “required employee contribution” to include on line 15 of Form 1095-C is the difference between the self-only amount the employer makes newly available to the employee under the individual coverage HRA for the month (the monthly HRA amount) and the employee’s monthly premium for self-only coverage under the lowest-cost silver plan offered in the Exchange for the rating area in which the employee resides (the PTC affordability plan).

Instead of using the Exchange where the employee resides, an employer may use a location-based safe harbor based on the employee’s primary worksite. In addition, employers may use a “look back” safe harbor to determine whether the premium for the lowest-cost silver plan self-only coverage should be determined by reference to the current or prior calendar year. Employers must apply the safe harbors on a consistent basis to all employees within a class. Employers may use a different safe harbor for different classes of employees.

Location-Based Safe Harbor

As mentioned, the “required employee contribution” to

include on line 15 of an employee’s Form 1095-C is the difference between the

self-only amount the employer makes newly available to the employee under the

individual coverage HRA for the month (the monthly HRA amount) and the employee’s

monthly premium for self-only coverage under the lowest-cost silver plan

offered in the Exchange for the rating area in which the employee resides

(the PTC affordability plan).

Under the location-based safe harbor, an employer may use the lowest-cost silver plan for self-only coverage through the Exchange where the employee’s primary site of employment is located. The employer is not required to use an employee’s actual residence to determine affordability unless the employee’s worksite is his or her home (due to remote or telecommute work). The primary site of employment is the location the employer expects the employee to perform services on the first day of the plan year or the effective date (the day the employee is eligible to participate in the ICHRA).

Age-Related Issues

The proposed regulations do not establish any specific safe harbors based on age; however, as a practical matter, an employer may use the age of the oldest employee to determine the ICHRA contribution for employees in that class (i.e., take the lowest-cost silver plan based on the age of the oldest employee). An employer may vary the amount of the ICHRA contribution based on age by no more than a 3:1 ratio between the oldest and youngest participant. An employer making age-based contributions may use the employee’s age on the first day of the plan year or the first day the employee is eligible to participate in the ICHRA.

Look-Back Month Safe Harbor

An employer may also utilize the look-back month safe harbor when selecting the lowest-cost silver plan. If the ICHRA operates on a calendar year basis, the employer may use the premium for self-only coverage under the lowest-cost silver plan from January of the prior calendar year. If the ICHRA operates on a non-calendar basis, the employer may use the monthly premium amount from January of the current calendar year. The difference in the look-back month is attributed to when the Exchange opens and when rates are submitted. The IRS understands that employers generally determine their plans and contributions ahead of time, and wants to ensure employers have the opportunity to make such determinations. If the employer chooses to use the look-back month safe harbor, the employer must use the employee’s current applicable location and current age, regardless of whether the lowest-cost silver plan is determined based on the current or prior year.

Example: Location and Look-Back Month Safe Harbor with Calendar Year ICHRA

For 2020, an employer offers all full-time employees and their dependents a calendar year ICHRA with $250 per month available regardless of family size. All employees have their primary site of employment in City A. An employee is 40 years old on January 1, 2020, and makes $15/hour. The applicable monthly premium for the lowest-cost silver plan for a 40-year old offered through the Exchange in City A for January 2019 is $400. The employer uses the Rate of Pay safe harbor for hourly employees.

In this example, the employee’s “required contribution” for each month of 2020 is the $150 difference between the lowest-cost silver plan ($400) and the employer’s monthly contribution ($250). Therefore, $150 is the amount reported on Line 15 of Form 1095-C.

Conclusion: ICHRA Contribution Results in an Affordable Offer

The employer has offered affordable coverage to this employee in 2020 because the required contribution ($150) is less than the Rate of Pay safe harbor for this employee (9.78% × $15 × 130 = $196).

Other Considerations

1094-C/1095-C Reporting

Applicable large employers are still required to perform the required employer mandate reporting (Forms 1094-C and 1095-C). The IRS indicated that reporting exceptions applicable to traditional HRAs integrated with fully insured group health plans will not apply. The IRS also indicated that additional guidance will be released before the calendar year 2020 reporting is due. If an employer offers affordable coverage under an ICHRA, it is presumed it meets minimum value and will be viewed as an offer of employer-sponsored group health plan coverage.

How to Find the Data

As a way to make determining affordability less burdensome, the proposed regulations state that for plans on the federal Exchange, the Department of Health and Human Services (HHS) has provided a platform for employers to view the lowest-cost silver plans in applicable locations. For plans offered through a state Exchange, the IRS stated that HHS will work with the states to implement a similar platform. If the employer uses the platform to determine affordability, it may rely on the information posted.

Section 105(h)

Nondiscrimination

An ICHRA, as a self-funded plan, is required to satisfy Section 105(h) nondiscrimination testing; however, an ICHRA that only reimburses insurance premiums and not medical expenses is not subject to Section 105(h). Although different classes are allowed, the ICHRA cannot discriminate in favor of highly compensated individuals. The proposed regulations provide that an ICHRA that satisfies the 3:1 age variation exception will not be discriminatory under Section 105(h) solely due to the variation based on age. Without the exception, Section 105(h) prohibits the maximum limit attributable to employer contributions to an HRA from being modified by reason of a participant’s age. The proposed regulations also provide that if the maximum dollar amount under an ICHRA varies for participants within a class of employees, or varies between classes of employees, then with respect to that variance, the ICHRA does not violate Section 105(h) so long as the maximum dollar amount only varies as permitted under the ICHRA rules.

Allowing Pre-Tax Contributions to Individual Market Coverage

The proposed regulations address the extent to which an employer can allow an employee to make pre-tax contributions towards his/her individual plan. The proposed regulations do not permit employees to take the salary reduction to purchase qualified health plans through the Exchange, which is expressly prohibited by the ACA. If an employee purchases an individual health plan off-Exchange (such as going directly to a carrier), an employer may allow employees to pay pre-tax for the portion of the premium not covered by the ICHRA. If an employer wants to allow pre-tax contributions, it must determine whether the individual coverage was purchased on-Exchange or off-Exchange, in order to determine if the deductions can be taken pre-tax.

What Employers Should Expect Next

Employers who are contemplating offering an ICHRA should consult with qualified ERISA counsel. There are additional requirements and guidelines an employer will need to meet in order to comply with all the requirements applicable to these new arrangements. The Departments also anticipate the release of additional guidance in the future.

__________________________________________________

About the Author. This alert was prepared by Stacy Barrow. Mr. Barrow is a nationally recognized expert on the Affordable Care Act. His firm, Marathas Barrow Weatherhead Lent LLP, is a premier employee benefits, executive compensation, and employment law firm. He can be reached at sbarrow@marbarlaw.com.

This email is a service to our clients and friends. It is designed only to give general information on the developments actually covered. It is not intended to be a comprehensive summary of recent developments in the law, treat exhaustively the subjects covered, provide legal advice, or render a legal opinion.

Benefit Advisors Network and its members are not attorneys and are not responsible for any legal advice. To fully understand how this or any legal or compliance information affects your unique situation, you should check with a qualified attorney.

© Copyright 2019 Benefit Advisors Network. All rights reserved.